House Money

What 2,000 wallets, a 98% win rate, and a $25 billion-a-month market tell us about the world we just rebuilt — without any of the guardrails we spent ninety years writing.

If you watched 60 Minutes on Sunday, you saw the cleanest case of insider trading anyone has put on television in a generation.

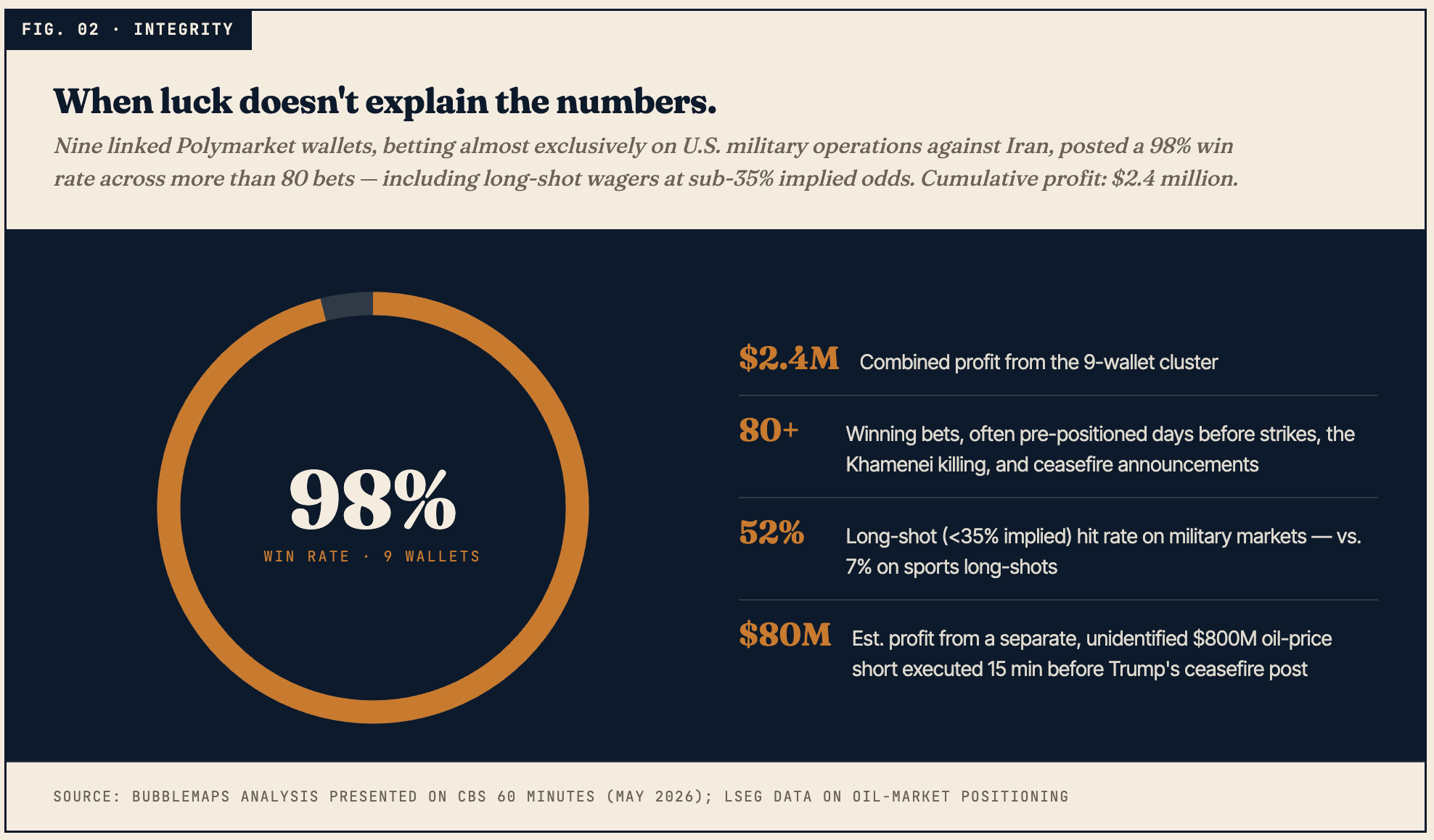

Nine wallets. Eighty-plus bets. A 98% win rate. Pre-positioned, in some cases days in advance, on the specific dates of the first U.S. strikes on Iran, the killing of Supreme Leader Ali Khamenei, and the announcement of the ceasefire. $2.4 million in profit. And — because this is Polymarket, which lives on a public blockchain — every wallet, every entry, every fill is sitting out in the open for anyone with a copy of Etherscan to walk through.

Bubblemaps, the small Paris analytics firm that found them, was blunt: “Luck alone cannot explain those numbers.”

What I want to do in this issue is not re-report the segment. CBS did the on-camera work, the Wall Street Journal did the distribution work two weeks earlier, the Times found dozens of additional suspicious clusters. The reporting is there. What I want to do is the part the reporting doesn’t quite get to, which is the part I happen to spend my working life thinking about: what does this look like from the perspective of someone whose entire job is regulated, audited, and surveilled?

Because from where I sit, what Polymarket and Kalshi are running is not a new financial product. It is an old one. It is the financial product that securities markets were before 1933.

I. The concentration

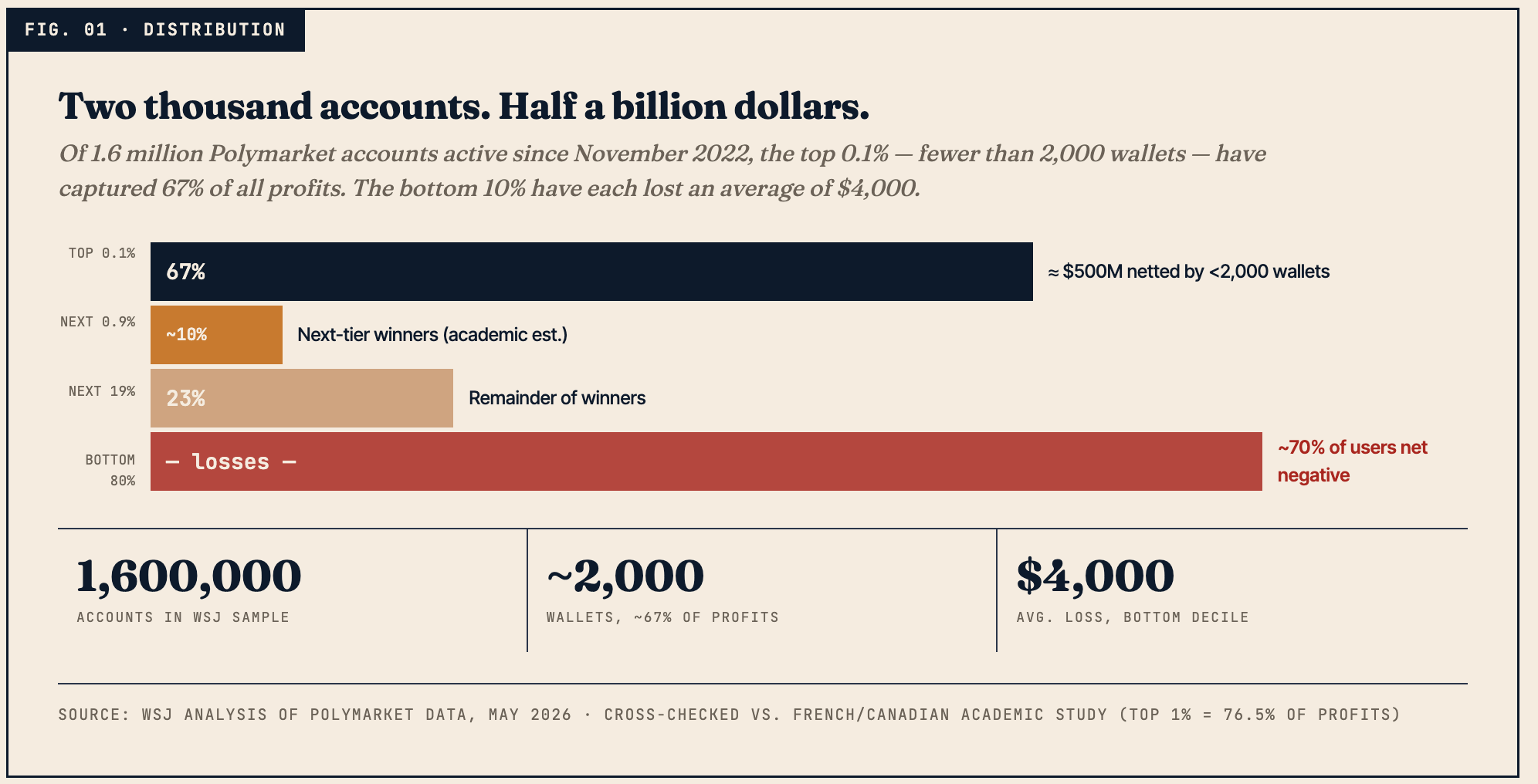

Start with the distribution, because the distribution is the whole story.

The Wall Street Journal pulled trade-level data on 1.6 million Polymarket accounts active since November 2022 — which, given the platform’s blockchain, is just a question of how much SQL you’re willing to write. They found that 0.1% of accounts captured 67% of profits. Roughly two thousand wallets, collectively netting close to half a billion dollars.

A separate academic study by researchers in France and Canada looked at a slightly different window and got a slightly more extreme number: top 1% of traders, 76.5% of gains. Pick whichever one you like; the shape is the same.

The bottom 10% of traders have lost an average of $4,000 each. The median user is somewhere between $1 and $100 in the red. About 70% of all participants lose money in aggregate.

Kalshi’s numbers, for the slice they disclose, are similar. Spokeswoman Elisabeth Diana told the Journal there are 2.9 unprofitable users for every profitable one. Their head of comms argued — accurately — that wealth concentration is common across financial markets, and that more Kalshi users make money than retail day traders or sports bettors do on traditional platforms.

That defense is true, and it is also the most damning thing anyone has said about prediction markets in print.

Because here’s the thing about that comparison. We know what equity markets look like when retail trades against professionals without rules: they look like the 1920s. The reforms that made it acceptable for a 401(k) participant to put their money next to a Renaissance Technologies trade — Section 10(b) of the Exchange Act, Rule 10b-5, Rule 14e-3, Reg FD, Reg SHO, exchange surveillance, FINRA, the SEC’s Office of Market Intelligence — that whole apparatus was built specifically so the distribution would not be what we are now seeing on Polymarket.

The 0.1% / 67% number isn’t a curiosity. It is what a market looks like before reform.

II. The mechanism

Now layer 60 Minutes on top.

The WSJ story is a distribution finding — who wins, who loses. It can’t, by itself, tell you why the winners win. There are at least three plausible explanations:

Genuine skill — like hedge fund manager dispersion, where the top decile actually is better at forecasting.

Capital and infrastructure — Susquehanna, Jump, and Citadel-affiliated market makers are reportedly running hundreds of millions a week through Kalshi. Of course they win; they make markets for a living.

Material nonpublic information — i.e., the thing that is a federal crime in equity markets.

The WSJ piece leans on the first two. The 60 Minutes piece pried open the third.

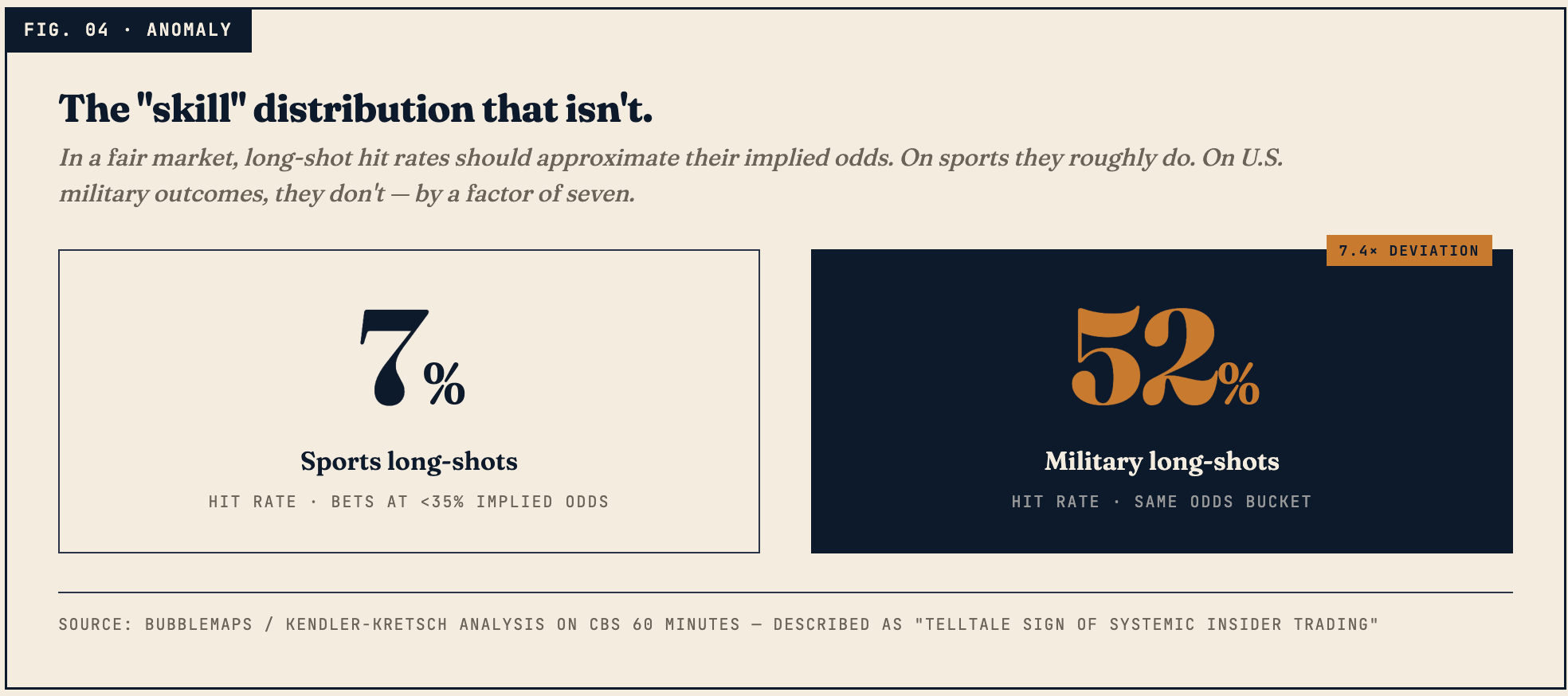

Take the long-shot test. In a fair market, bets at sub-35% implied odds should hit roughly 35% of the time. On Kalshi sports markets, Bubblemaps found, they hit 7% — which is actually consistent with retail buying overpriced lottery tickets, the standard “favorite-longshot bias” you see in every parimutuel betting pool ever studied.

On the military outcome markets, those same long-shots hit 52% of the time.

There is no theory of skill that gets you from 7% to 52% in a market with binary, externally-resolved outcomes by changing the topic. There is exactly one theory that gets you there, and Bubblemaps’ analyst gave its name on national television: systemic insider trading.

The 9-wallet cluster is the headline, but the more disturbing finding is the broader anomaly. The cluster is what they could prove. The 52% number is what the market structure looks like in aggregate.

And then there is the trade no one has yet pinned to a name. At 6:50 a.m. on a morning in June, more than $800 million was staked on oil prices dropping. Fifteen minutes later, the President posted on Truth Social that the White House and Iran had “very good and productive” conversations about ending hostilities. Oil fell more than 10%. The position was worth, by LSEG’s reconstruction, somewhere in the neighborhood of $80 million in profit. Federal investigators are reportedly probing the trades. No charges have been filed.

The sources 60 Minutes spoke to noted, in the careful way you have to note these things on television, that the trader could have been domestic. Or foreign. Or — in the head of Bubblemaps’ investigations team’s phrasing — an enemy.

This is what people miss when they roll their eyes at “prediction markets are gambling.” The problem is not that some retail user lost $5,000 betting on whether a celebrity would say a word. The problem is that the platform has now become a liquid, anonymous, on-demand market for monetizing classified information, including national security information, where the front-running is so flagrant a French startup with twelve people can find it on a Tuesday.

III. The expected value, for the people you and I actually know

The mention markets are the part that makes me angriest, so I want to spend a paragraph on them.

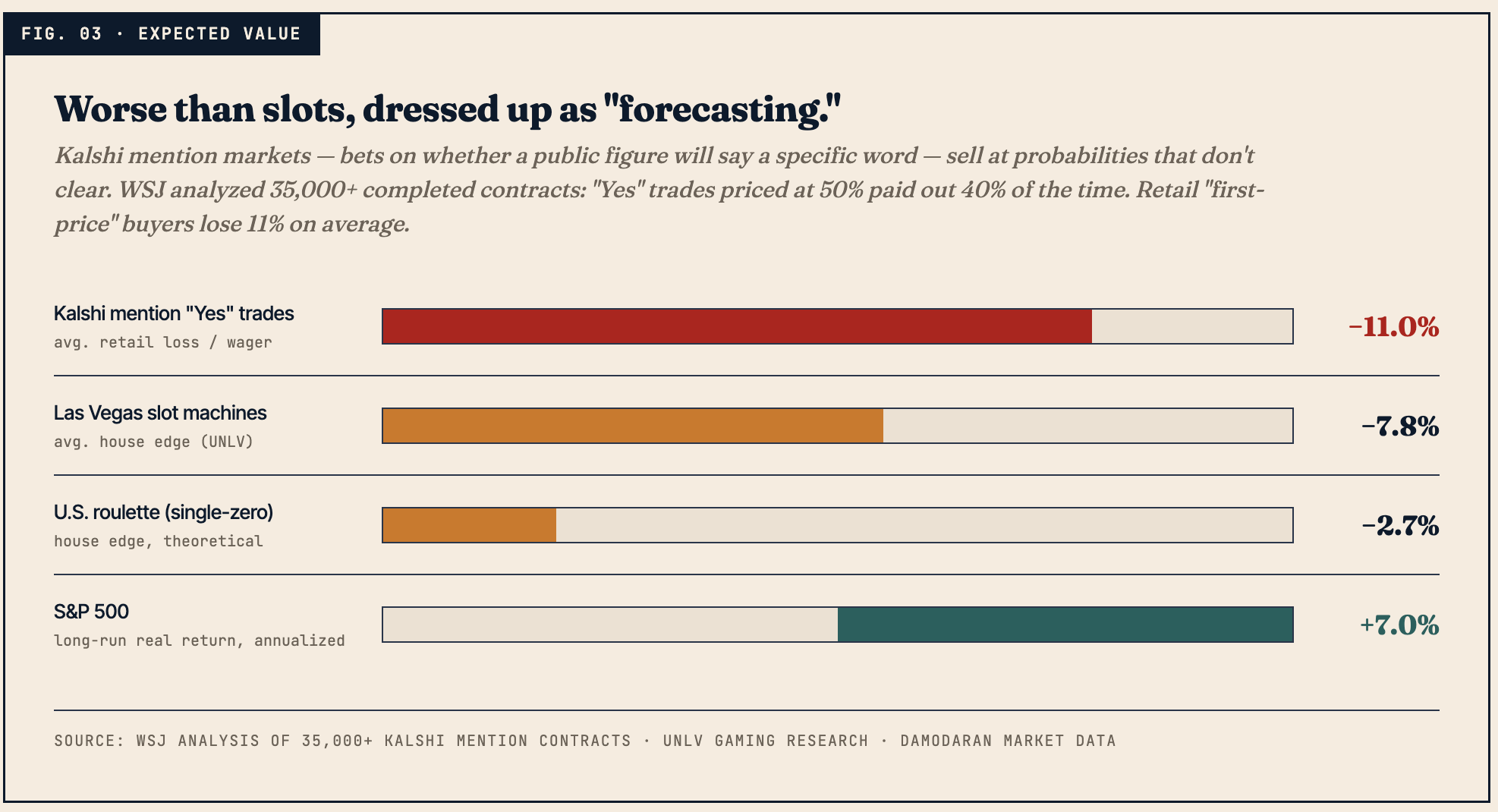

Kalshi runs contracts on whether a specific public figure will utter a specific word during a specific televised appearance. The Journal analyzed 35,000 of them. They found that “Yes” contracts priced at a 50% probability paid out about 40% of the time — meaning retail buyers, on average, lose 11% of whatever they wager on first-price entry.

A Las Vegas slot machine, per University of Nevada gaming research, has a house edge of roughly 7-8%.

Kalshi’s mention markets are worse than slots, and they are marketed with TikTok testimonials about a woman who “got two years of rent” through Kalshi’s predictions and a 33-year-old former Outback Steakhouse line cook in Detroit who turned $2,000 into $41,000, then lost all of it on one celebrity mention. The Journal found him; his story is in the piece.

Professional traders, asked by reporters, said they don’t touch these markets. They are “unpredictable” — i.e., they are negative expected value even for the smartest people on the platform, because the prices are set wrong relative to the underlying probabilities, and the only people consistently buying are retail. That is the textbook definition of a market that exists to transfer wealth in one direction.

IV. The regulatory frame, which is the part of this story I cannot stop thinking about

Here is the thing that, working in a regulated corner of financial services every day, I find genuinely hard to process.

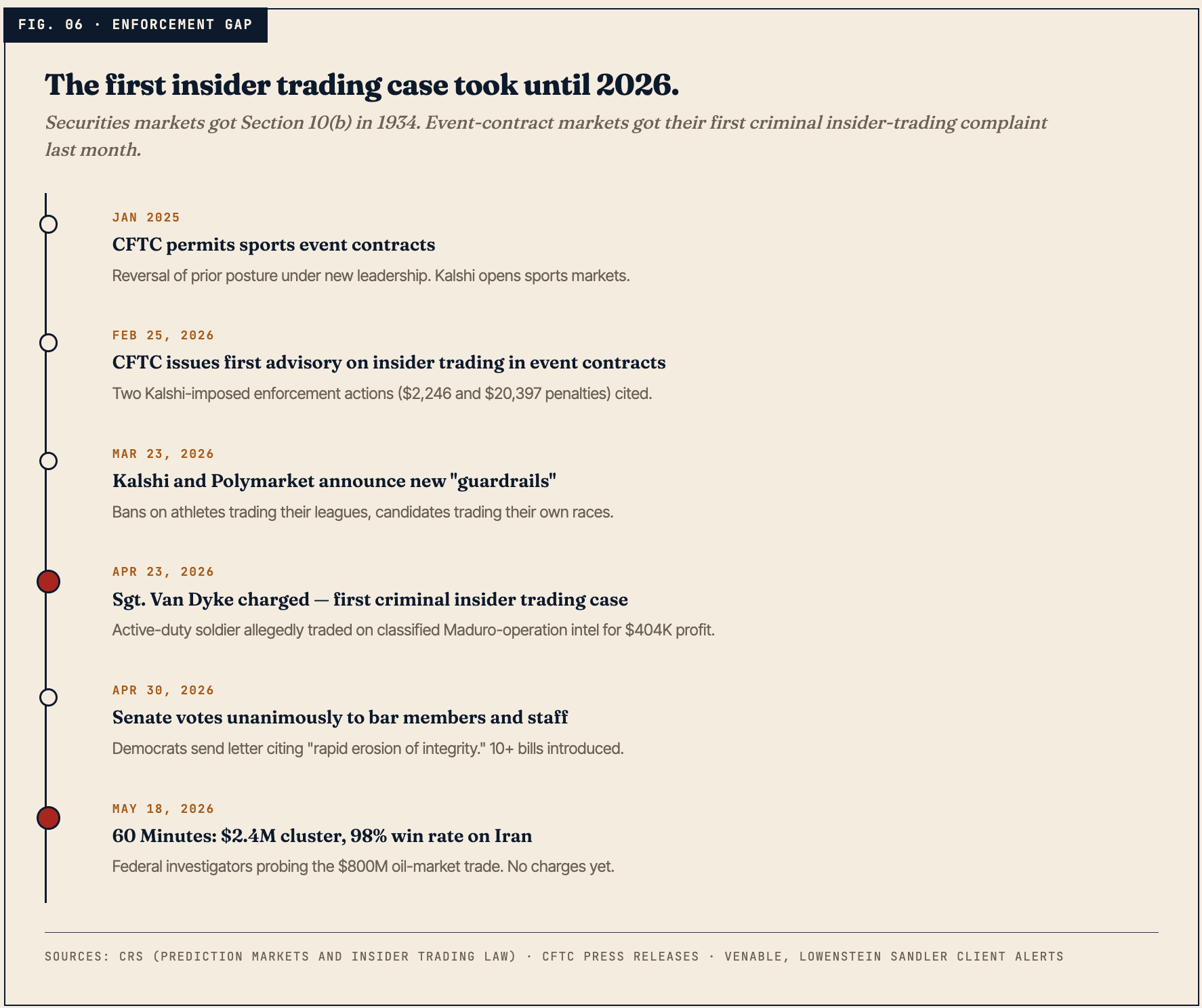

The first criminal insider trading complaint involving an event contract was filed on April 23, 2026.

That’s it. That’s the whole enforcement history. One case — Sgt. Gannon Ken Van Dyke, who allegedly used classified intelligence about the Maduro operation to net $404,000 on Polymarket, then asked the platform to delete his account when the bet hit. The CFTC charged him a month ago.

For comparison, the Securities and Exchange Act of 1934 — the law that gives the SEC its insider-trading authority — was enacted ninety-two years ago, in response to a market crash that erased $30 billion in nominal wealth (roughly $700 billion today). Rule 10b-5 was adopted in 1942. Rule 14e-3, governing tender-offer trading on MNPI, came in 1980. Reg FD, which made selective disclosure to favored analysts illegal, came in 2000.

We built that apparatus piece by piece, over decades, after watching what happens when you don’t have it. We built it because the alternative — what happens when sophisticated traders can act on private information against retail counterparties with no recourse — was a wealth-extraction machine that nearly killed American capitalism.

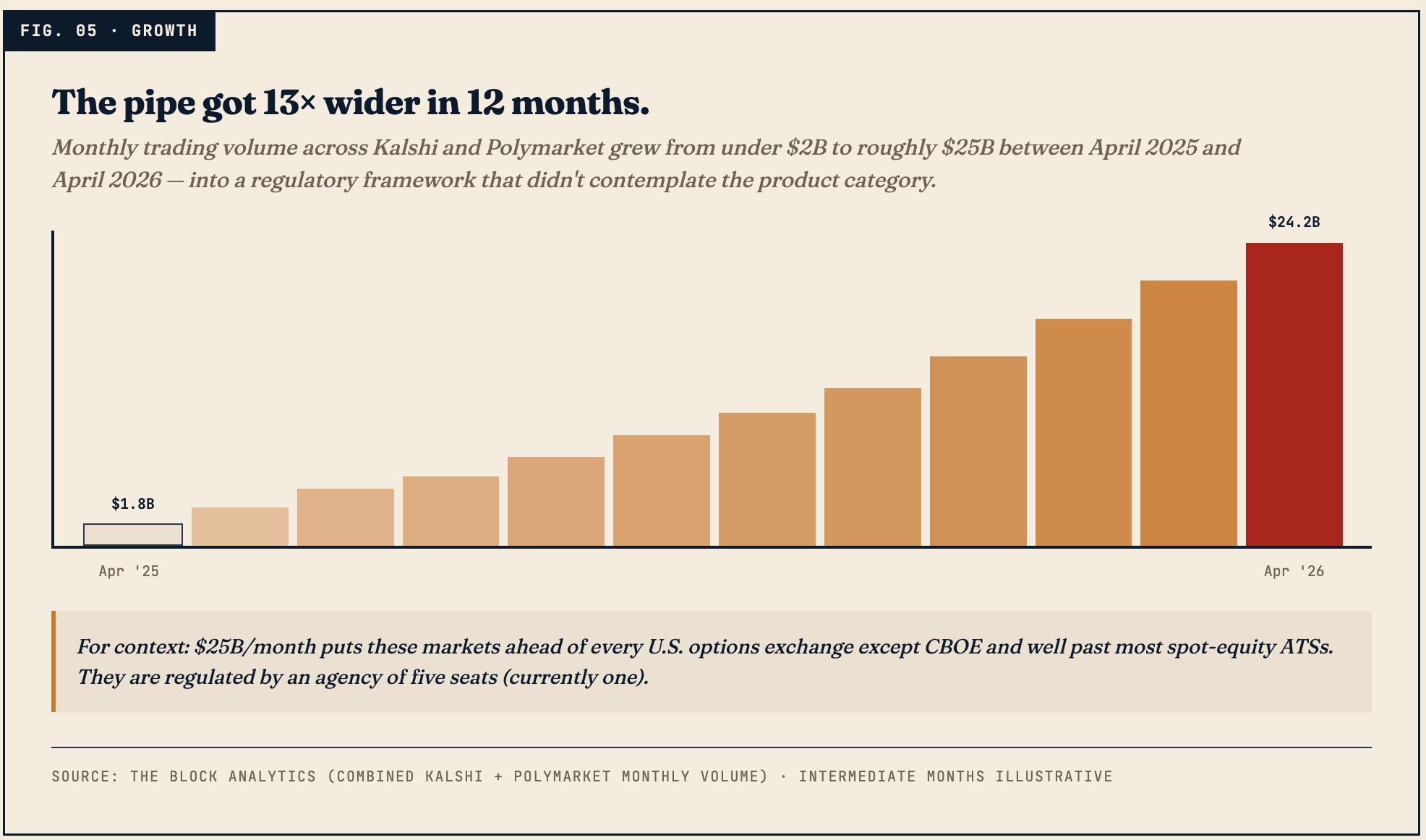

And then, starting in early 2025, the CFTC reversed its prior posture on event contracts and the market grew 13x in twelve months, from $1.8 billion in monthly volume to $24.2 billion, and the framework that we use to police it is:

One CFTC commissioner (the commission is statutorily five seats; four are vacant)

Rule 180.1, which is modeled on Rule 10b-5 but has never been tested in this context

A six-page advisory letter from February

Whatever rules each individual platform decides to write for itself

The fact that Polymarket’s main exchange is offshore and “claims to block U.S. users”

The CFTC was set up in the 1970s to regulate commodity futures and food prices. It is being asked to police a $25-billion-a-month derivatives market on national security outcomes with one seated commissioner and a staff advisory.

The platforms themselves have done some things — Polymarket signed a deal with Chainalysis for blockchain surveillance and with Palantir for AI monitoring; Kalshi opened more than 200 internal insider-trading investigations and has actioned a dozen. Polymarket revised its rulebook in March to bar trading on “information that would violate a preexisting duty or obligation of trust or confidence.”

But the fines are the part that gives the game away. Kalshi’s enforcement against the candidate who bet on his own race was a $2,246 penalty. Against the YouTube channel editor with apparent advance access to the channel’s content: $20,397. These are not enforcement actions. These are the cost of doing business if you happen to get caught.

The CEO of Polymarket told an Axios audience last fall that insider trading “is sort of an inevitability” and that “there’s a lot of benefits from it.” The benefit, he said, is that it creates a financial incentive for insiders to “divulge information to the market.”

That is, again, true. It is also the literal opposite of the rule we wrote ninety-two years ago.

V. So what is this, actually

The honest answer is that prediction markets, as currently constituted, are three things wearing one trenchcoat:

One: A genuinely useful price-discovery mechanism for forecastable events, of the sort academics have advocated for since Hanson and Hahn and the Iowa Electronic Markets in the late 1980s. There is real informational value in a liquid market on, say, central bank decisions. I am not an opponent of the concept.

Two: An unregulated securities exchange. A market for binary contracts on outcomes that often are tradable in regulated venues (FOMC, NFP, election outcomes have been tradable via futures, options, and structured products for years), now offered with no MNPI rules, no disclosure regime, no surveillance worth the name, and a 11% house take that exceeds Vegas.

Three: A monetization layer for classified information, both domestic and foreign, where the front-running is so blatant that a French analytics firm can identify $2.4M clusters from a coffee shop.

The first one is worth defending. The second and third are why every reform-era financial historian I know is having quiet panic attacks.

And the structural growth case is enormous. Kalshi is raising at a $22 billion valuation with a $1B+ revenue run rate; Polymarket is in talks at $15 billion. Susquehanna, Jump, and Citadel-affiliated firms are providing the liquidity that makes the 0.1%/67% number work. ICE has committed up to $2 billion to Polymarket. Both platforms are expanding into perpetual futures — continuous-duration contracts that will compound the retail-vs-pro asymmetry indefinitely.

This is going to be a major asset class. The question is whether it gets the 1934 treatment now, or whether we wait for the cracking sound first.

What I’d actually like to see (and what I think actually happens)

The serious reforms are not hard to write. We have ninety years of practice. Off the top

Rule 10b-5 equivalent applied via CFTC Rule 180.1 with explicit MNPI definitions

A Reg FD analog for event-market issuers (campaign staff, league officials, federal employees) requiring simultaneous public disclosure or trading bars

Position-limit and large-trader reporting on contracts above a notional threshold (the $800M oil trade should not be anonymous after the fact, much less in real time)

Mandatory KYC for any wallet above some de minimis lifetime volume on U.S.-accessible platforms

An outright prohibition on contracts referencing classified U.S. military operations

A statutory ban on federal employees and their immediate families, with the same teeth the STOCK Act has (or, more honestly, with teeth the STOCK Act should have had)

What I think actually happens, given the current political configuration and the fact that Donald Trump Jr. is both an investor in Polymarket and a strategic advisor to Kalshi: a federal preemption framework that papers over the worst abuses with platform self-regulation, leaves the state regulators boxed out, and treats the CFTC as the lead agency for a product set that probably belongs at the SEC. The Senate just voted unanimously to bar its own members and staff from trading prediction markets, which is a tell about where the political risk is perceived to be and which problem actually gets fixed first.

The retail loss machine will keep running. The 0.1% will keep winning. The cluster of nine wallets with the 98% Iran win rate may or may not be charged — federal investigators are still working it, per CBS — and the $800M oil trader is, for now, just a line in an LSEG dataset.

If you found this useful, the deeper version is below — paid subscribers get the institutional-arbitrage piece: how a CFTC-regulated venue with no MNPI rules and $25B/month in volume changes the calculus for actual hedge fund and reinsurance counterparties (yes, reinsurance — there’s a transferred-risk angle worth a whole post), what the on-chain forensic playbook actually looks like, and which six contract categories I expect to be banned or position-limited within 18 months.

Founding members get the model file (Polymarket flow concentration by contract type, mapped against my framework for “what should and shouldn’t trade in an unrestricted venue”).

Adaptive Asset Analytics writes the institutional reinsurance perspective on markets and sport. If you got this from a friend, the subscribe button is below. — Adam

Sources

Wall Street Journal, “Just 0.1% of Polymarket accounts captured 67% of all profits” (May 4, 2026)

CBS 60 Minutes, “Online prediction market traders make millions betting on U.S. military operations” (May 17, 2026); Bubblemaps investigation by Nicolas Vaiman and “Deebs”

New York Times, “Dozens of Polymarket Bets Show Signs of Insider Trading” (May 2026)

Congressional Research Service: LSB11406 (Prediction Markets and Insider Trading Law); IF13187 (Prediction Markets: Policy Issues for Congress)

CFTC Press Release No. 9217-26 (Van Dyke complaint, April 23, 2026); Staff Advisory No. 26-08

Lowenstein Sandler client alert (April 2026); Venable LLP analysis (April 2026); Herbert Smith Freehills Kramer (May 2026)

NPR, “Campaign staffers tell NPR they make ‘thousands’ betting on their own candidates” (May 7, 2026)